Notion's Path From Frothy Valuation to Public Company

Press Space for next Tweet

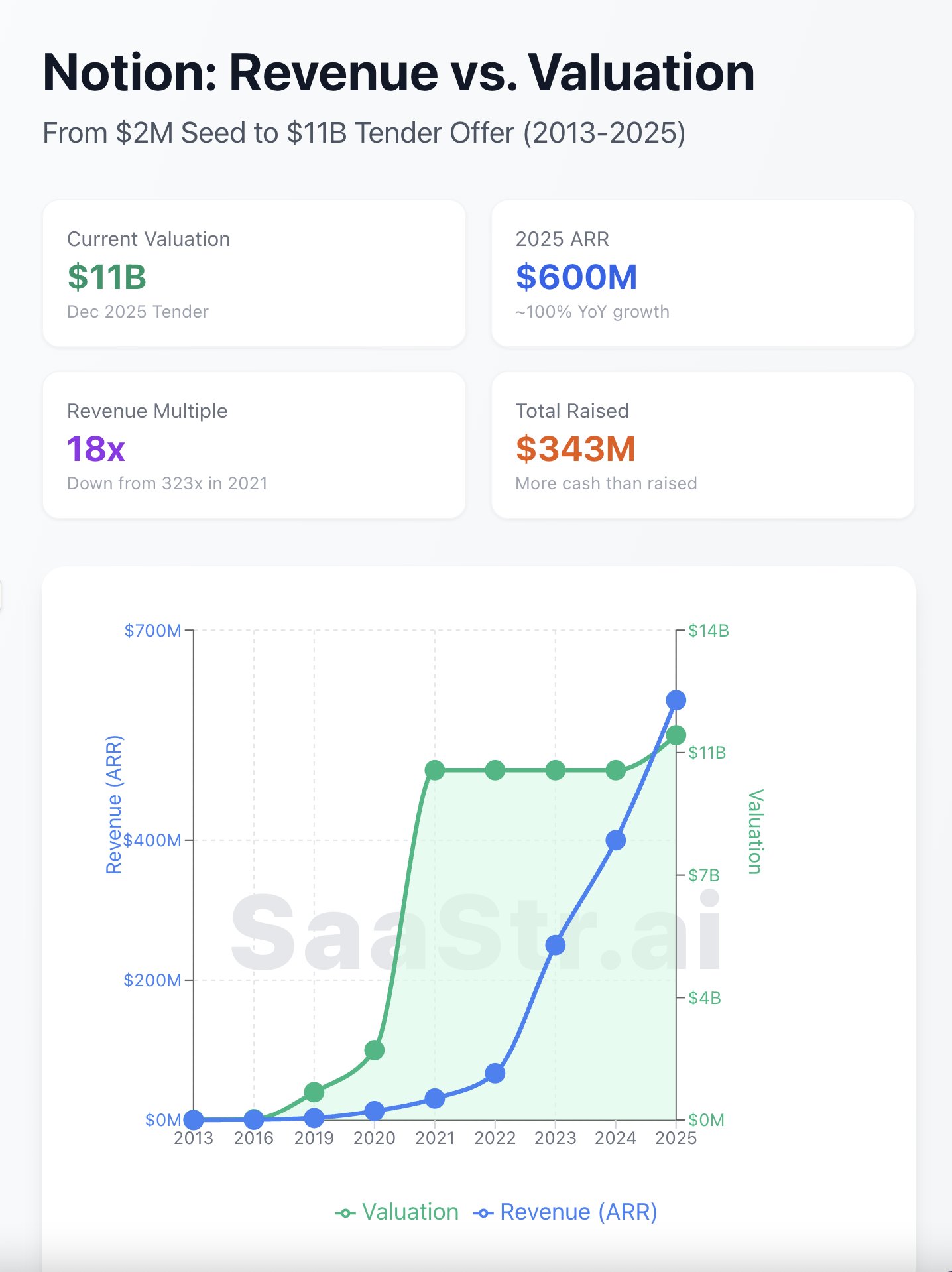

Notion: $2M seed → $11B in 12 years. A great case study on growing into your valuation The journey: 2013: $2M seed 2019: $3M ARR → $800M val (267x) 2020: $13M ARR → $2B val (154x) 2021: $31M ARR → $10B val (322x) ← peak ZIRP froth 2022: $67M ARR → $10B val (149x) 2023: $250M ARR → $10B val (40x) 2024: $400M ARR → $10B val (25x) 2025: $600M ARR → $11B val (18x) ← today Revenue grew 19x in 4 years. Valuation moved 10%. That's how you fix a stretched multiple—you don't. You outgrow it. The AI kicker: 50%+ of customers now pay for AI eatures, up from 10-20% last year. They bundled AI into Business/Enterprise tiers. Smart. At 18x ARR with ~100% growth, Notion is priced like a public company already. That's conservative for a PLG rocket ship doubling annually. IPO likely late 2026. At this pace, $1B+ ARR by then. Could support $15-20B+ public market cap. The playbook: Raised at the peak (Oct 2021 at 322x Didn't need to raise again—they have more cash than the $343M raised Let revenue catch up to valuation Go public when fundamentals align Ivan Zhao still owns 30%. No VCs on the board. Patience wins.

Topics

Read the stories that matter.The stories and ideas that actually matter.

Save hours a day in 5 minutesTurn hours of scrolling into a five minute read.